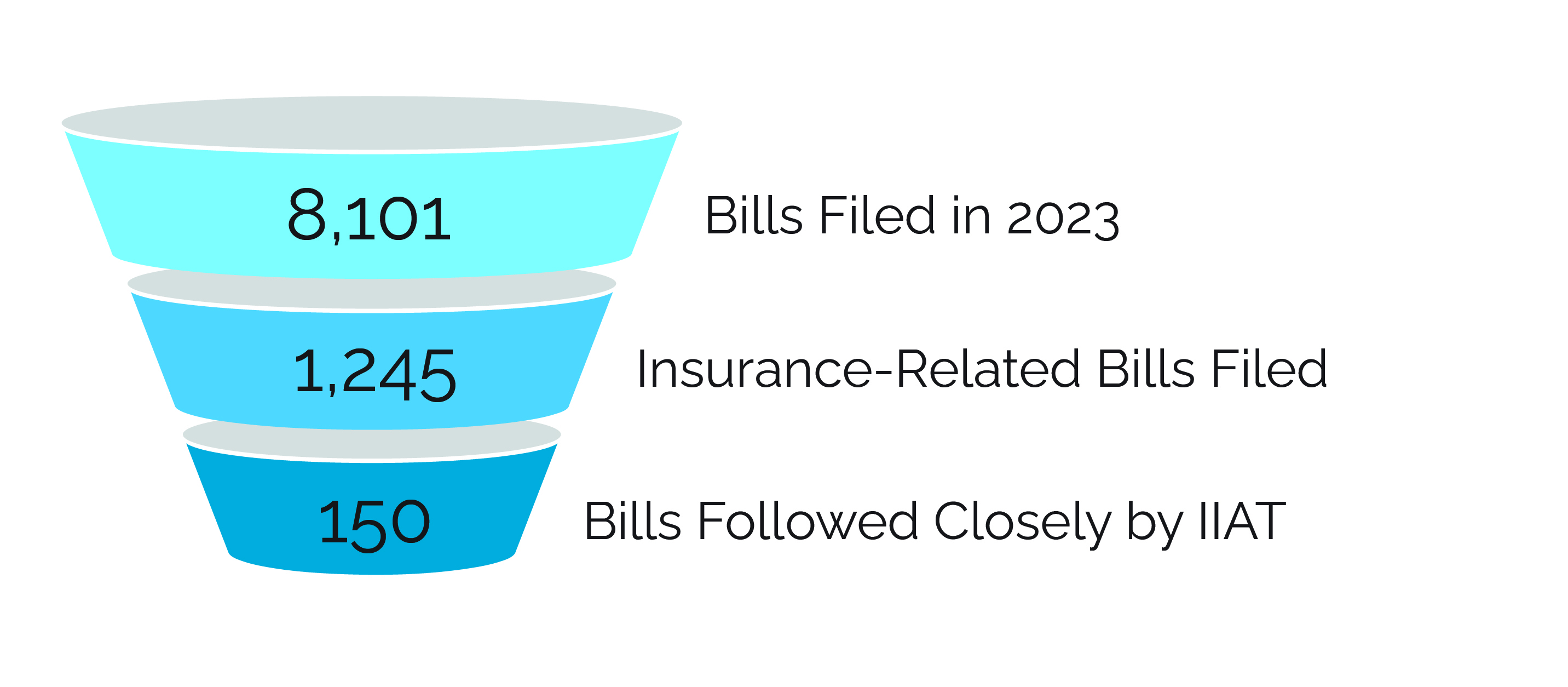

A look back at recent Texas Legislative Sessions by the Numbers

View IIAT's Key Legislation & Bills of Interest for the 88th (2023) Texas Legislative Session

View IIAT's Key Legislation & Bills of Interest for the 88th (2023) Texas Legislative Session